ESG Insights: Choosing the right ESG reporting standard for your company

- Post Date

- 19 May 2022

- Read Time

- 4 minutes

Environmental, Social, and Governance (ESG) reports, also known as “disclosures”, vary dramatically from company to company in terms of length, format, topics covered and depth of coverage. This can be confusing to companies and their stakeholders. Why is there so much variety?

First, ESG reporting is voluntary in many countries, so there is no one standard mandated by the government in those countries. Instead, there are dozens of ESG reporting standards, most of which are international, developed and managed by private entities. Each of these private entities has taken a slightly different approach to what is important in ESG disclosure.

There are three general types of ESG standards:

- questionnaires,

- leveraged information reports, and

- reporting frameworks.

Questionnaire standards do not require the disclosing company to write a report but only respond to a set of questions tailored to the industry. One of the first widely used ESG questionnaire standard was the CDP (formerly the Carbon Disclosure Project). Questionnaire standards are deceptively simple. While there is no pressure to craft an individual report, the questions are challenging and aimed towards generating a high degree of disclosure from companies.

Leveraged information reports, such as the Newsweek Green Rankings, are “reverse reports” in that the standard operator performs research on a company, which is often unflattering, then prepares a report to present to the company with an “invitation” to respond with changes before the report is published. Defending against unflattering statements in these reports is often a company’s first experience with ESG disclosure.

Reporting frameworks provide detailed guidelines specific to key industries that a company can use to write its own report. Typically, these frameworks offer flexibility in how deeply the topics in the guideline must be covered, allowing for a wide range of disclosure results. Of the three types of ESG standards, the most popular is the reporting framework.

The two most widely used ESG reporting frameworks, which can be applied to most any business, are the Sustainability Accounting Standards Board (SASB) and Global Reporting Initiative (GRI) frameworks. SASB and GRI approach ESG from significantly different perspectives and, as a result, companies frequently use both to be highly inclusive.

The SASB perspective is focused on how ESG standards affect a company’s financial condition, operating performance, and risk profile. SASB can even be used to combine a company’s annual financial report and ESG report into one document.

The GRI perspective is focused on how ESG standards affect a company’s environmental and social contributions and style of self-governance (both positive and negative). The GRI framework tasks a company with identifying those issues that are of primary importance to an organisation’s stakeholders (called material issues) and disclosing the ESG impacts of these issues.

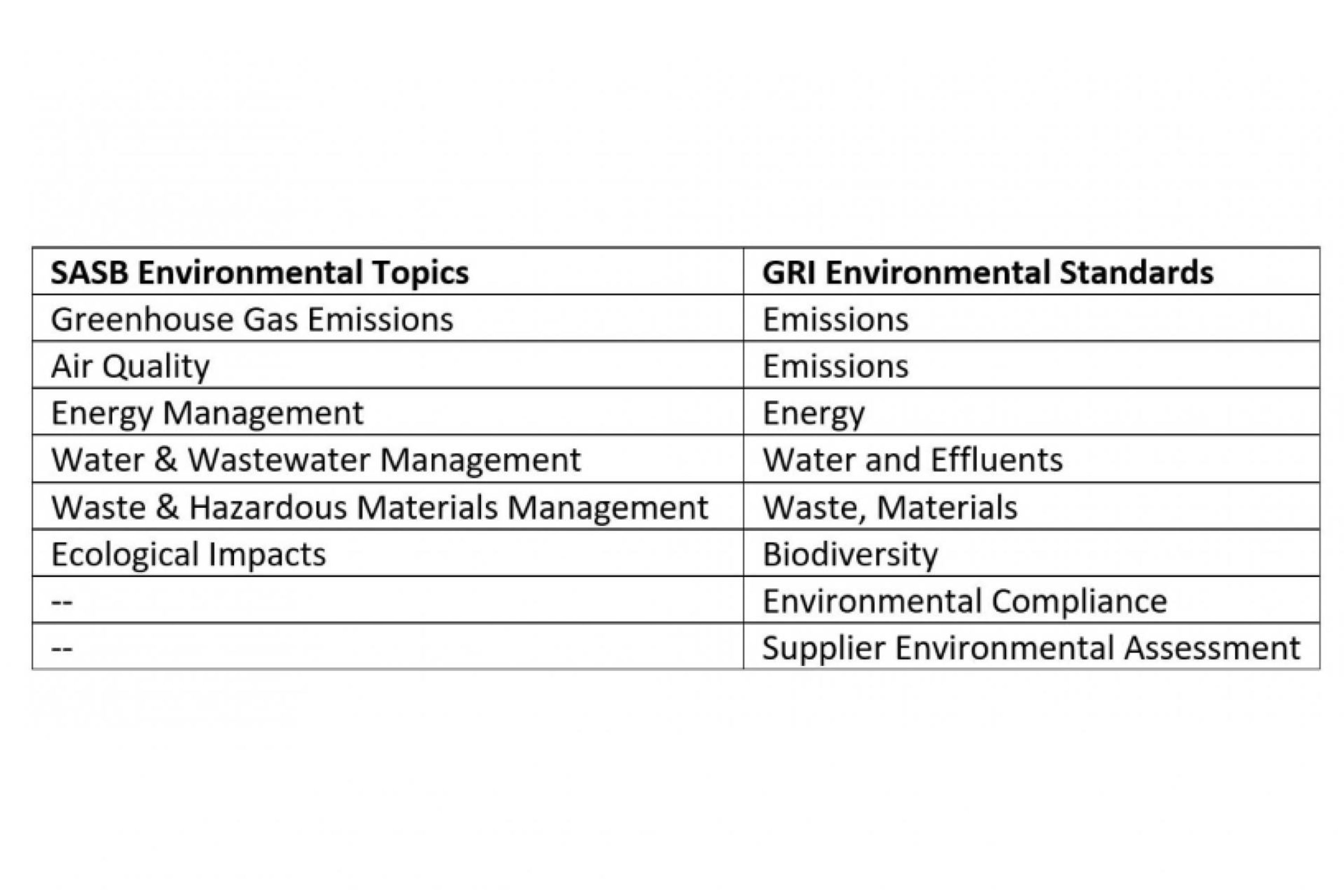

Even with their differing sustainability disclosure perspectives, the SASB and GRI standards have common ground for measuring the environment performance of organisations, as shown in Table 1.

Table 1. Comparison of selected SASB and GRI Indicators for ESG Reporting.

As shown, greenhouse gas emissions, air quality emissions, energy, water use and wastewater, materials and waste management, and biodiversity indicators are highlighted within both the SASB and GRI sustainability disclosure frameworks.

The importance or level of risk that any one environmental indicator carries for a given organisation depends on the organisation’s industry sector, regional regulations, stakeholder interest, and business strategy.

Beyond SASB and GRI, there also exist numerous specialised ESG reporting frameworks. One such specialised ESG reporting framework is the Task Force on Climate-Related Financial Disclosures (TCFD). This standard focuses specifically on the risks and opportunities triggered for a company by climate change and the financial implications to the company of these risks and opportunities.

Another example of a specialized ESG reporting framework is the International Petroleum Industry Environmental Conservation Association (IPEICA) which only applies to companies in the oil and gas business.

SLR’s ESG team collaborates with companies tackling ESG reporting to help them identify which ESG standard(s) work well within their industry and with their particular corporate management system. SLR has the experience to help companies choose the right standards for their company the first time they report and develop strategies for improving disclosure over time.

Recent posts

-

-

-

Navigating the evolving landscape of corporate sustainability and communications in the US

by Chynna Pickens

View post